- Introduction

- What Is a Pension Company in Nigeria?

- What Pension Companies (PFAs) Do in Nigeria

- 1. Collect Contributions

- 2. Invest Your Money

- 3. Keep Accurate Records

- 4. Pay Retirement Benefits

- 5. Provide Customer Support and Financial Guidance

- Examples of Pension Companies in Nigeria

- Risks Associated With Pension Companies

- Benefits of Using a Pension Company

- Why Pension Companies Matter in Nigeria

- What Makes a Pension Company “Low Fee”?

- Understanding Growth Potential in Nigerian Pension Funds

- Key Features to Look For in a Good Nigerian Pension Company

- Top Nigerian Pension Companies With Low Fees and High Growth (2025 Review)

- Comparison Table: Low Fees vs Growth Potential

- Benefits of Choosing a Low-Fee, High-Growth PFA

- Who Should Choose These Types of PFAs?

- Common Mistakes Nigerians Make When Choosing a PFA

- How to Switch to a Better Pension Company in Nigeria

- Frequently Asked Questions (Nigeria Edition)

- 1. Do pension fees really affect my retirement savings?

- 2. Can low-fee PFAs still perform well?

- 3. How do I know if my PFA is doing well?

- 4. How often should I check my pension?

- 5. Is it safe to choose aggressive growth funds?

- Conclusion

Introduction

Planning for retirement is one of the smartest financial decisions anyone in Nigeria can make today. Whether you are a salary earner, self-employed, a civil servant, or a small business owner, the pension company you choose now will strongly influence the quality of your life when you finally stop working.

For many Nigerians, the biggest challenge is finding a pension provider that does not charge high fees but still delivers strong long-term returns. Even small fees, when deducted year after year, can quietly reduce your retirement savings without you noticing.

What Is a Pension Company in Nigeria?

A pension company in Nigeria officially called a Pension Fund Administrator (PFA) is a licensed organization that helps you:

- Save money for retirement

- Manage your monthly pension contributions

- Invest your funds so they can grow steadily over time

- Pay you after retirement

When you retire, the pension company ensures you receive either a lump sum, a monthly pension, or both, depending on the size of your Retirement Savings Account (RSA).

What Pension Companies (PFAs) Do in Nigeria

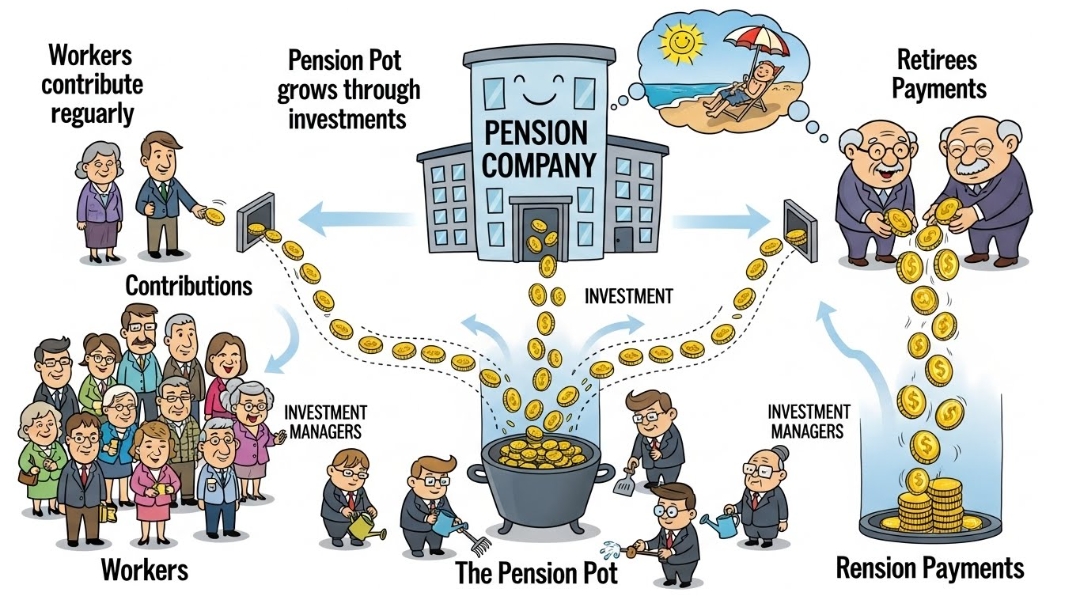

1. Collect Contributions

PFAs receive monthly payments from your employer and sometimes from you directly (especially if you are self-employed under the Micro Pension Plan).

2. Invest Your Money

They invest your retirement funds in assets like government bonds, Nigerian stocks, real estate, corporate bonds and money market instruments with the aim of growing your money over time.

3. Keep Accurate Records

PFAs track your RSA balance, monthly contributions, investment returns and withdrawal status.

4. Pay Retirement Benefits

Once you reach retirement age (or qualify under early retirement rules), the PFA pays your pension.

5. Provide Customer Support and Financial Guidance

Some PFAs offer retirement planning tools, mobile apps and financial advice.

Examples of Pension Companies in Nigeria

Some well-known PFAs regulated by PENCOM include:

- Stanbic IBTC Pension

- ARM Pensions

- Leadway Pensure

- Premium Pension

- FCMB Pensions

- CrusaderSterling Pensions

While global names like Vanguard and Fidelity are familiar internationally, Nigerians should always choose PFAs licensed and regulated by PENCOM.

Risks Associated With Pension Companies

Market risk: investments can fall in value during downturns.

Inflation risk: returns may not keep pace with rising prices.

Operational risk: poor management can reduce returns.

Insufficient contributions: low deposits lead to inadequate retirement income.

Benefits of Using a Pension Company

There are several benefits of using pension companies in Nigeria, and these include:

- Financial security in retirement

- Long-term investment growth

- Employer contributions that boost savings

- Regulatory protection under PENCOM

- Tax advantages where applicable

Why Pension Companies Matter in Nigeria

In a country where many people rely on family support after retirement, a pension plan provides:

- Financial independence

- Stability in old age

- A buffer against inflation and healthcare bills

- Reduced pressure on family members

Your pension is your future salary so choosing the right PFA is essential.

What Makes a Pension Company “Low Fee”?

Every pension company charges fees to manage your account, but the amounts differ. These fees can look small, but they reduce your long-term returns significantly if they are too high.

Common Pension Fees in Nigeria

- Fund Management Fee

- Administrative Fee

- Annual Maintenance Fee

- Transfer or Exit Fee (if switching companies)

- Fund Switching Fee

Why Low Fees Matter

Imagine two pension companies one charges 0.5% and another charges 2%. Over 20–30 years, that difference can reduce your final retirement savings by millions of naira.

How to Identify Low-Fee Pension Providers

- Compare published fee schedules

- Read your RSA statements carefully

- Avoid PFAs with unexplained deductions

- Review independent PENCOM reports

- Check customer reviews online

Transparency is key. If their charges are unclear, consider other options.

Understanding Growth Potential in Nigerian Pension Funds

A pension company with high growth potential invests your money wisely and consistently delivers strong long-term returns.

Factors That Influence Growth Potential

- Investment Strategy: Diversified portfolios generally perform better.

- Historical Performance: Look for consistent 5–10 year returns.

- Risk Management: The best PFAs balance growth and safety.

- Economic Expertise: Understanding inflation, FX and interest trends helps.

- Corporate Governance: PENCOM compliance protects your savings.

Growth vs Risk

High growth potential does not automatically mean reckless risk. Well-managed funds pursue long-term performance rather than short-term speculation.

Key Features to Look For in a Good Nigerian Pension Company

- Low and Transparent Fees no hidden charges.

- Strong Investment Returns review long-term performance reports.

- Multiple Fund Choices Fund I (aggressive) to Fund IV (retirees) and Micro Pension options.

- Reliable Customer Support phone, email, WhatsApp or app.

- Digital Tools mobile app, calculators and online statements.

- PENCOM Compliance only pick regulated PFAs.

Top Nigerian Pension Companies With Low Fees and High Growth (2025 Review)

Below is an adapted review for Nigeria, based on the general performance indicators and industry reputation. You can as well expand or update this list with specific recent performance data.

Stanbic IBTC Pension Managers

Overview: One of Nigeria’s largest PFAs with a strong long-term track record.

Fees: Competitive and transparent.

Growth Potential: Historically stable returns across most fund types.

Best For: Young earners, corporate workers and high-income earners.

ARM Pensions

Overview: Known for strong investment strategy and digital innovation.

Fees: Transparent with low admin charges.

Growth Potential: Strong 10-year performance.

Best For: Professionals seeking consistent long-term returns.

Leadway Pensure

Overview: Reliable customer service and strong governance culture.

Fees: Low compared to many PFAs.

Growth Potential: Balanced portfolio with steady growth.

Best For: Risk-averse savers and pre-retirees.

Premium Pension Limited

Overview: Popular for a diversified investment approach.

Fees: Competitive and clearly disclosed.

Growth Potential: Notable performance in Fund II and Fund III.

Best For: Middle-aged workers and civil servants.

FCMB Pensions

Overview: Good for people who value mobile tools and ease of access.

Fees: Among the lowest in the industry.

Growth Potential: Strong returns, especially in growth funds.

Best For: Young professionals and self-employed Nigerians.

Comparison Table: Low Fees vs Growth Potential

| Pension Company | Annual Fees | Admin Charges | Historical Returns | Best For |

|---|---|---|---|---|

| Stanbic IBTC | Low | Transparent | High | Young earners |

| ARM Pensions | Low | None | High | Professionals |

| Leadway Pensure | Low | None | Moderate | Pre-retirees |

| Premium Pension | Low | Few | Moderate–High | Civil Servants |

| FCMB Pensions | Very Low | Transparent | High | Self-employed |

Benefits of Choosing a Low-Fee, High-Growth PFA

- Faster Compounding: More of your money stays invested.

- Higher Retirement Income: You keep more of your savings.

- Less Financial Stress: Easier to plan with confidence.

- More Flexibility: Better fund-switching and contribution options.

- Wealth Preservation: Lower deductions mean more wealth saved.

Who Should Choose These Types of PFAs?

These PFAs suit:

- Young workers who want long-term compounding

- Mid-career employees maximizing savings

- Self-employed individuals under the Micro Pension Plan

- High-income earners making large voluntary contributions

- Small business owners managing staff pensions

- People aiming for early retirement

Common Mistakes Nigerians Make When Choosing a PFA

- Ignoring fee structures and hidden charges

- Relying on popularity instead of performance

- Not reviewing performance at least once a year

- Focusing only on short-term returns

- Not matching fund types to age and goals (e.g. young people in Fund III/IV)

How to Switch to a Better Pension Company in Nigeria

Switching is your legal right under PENCOM regulations. Follow these steps:

- Compare fees and performance of PFAs you’re considering.

- Contact the new PFA and request a transfer form.

- Complete the transfer request and submit your RSA PIN and ID.

- Wait for the transfer timelines vary from 2 to 12 weeks depending on the process.

Before switching, check for any exit fees, transfer restrictions and the quality of customer service.

Frequently Asked Questions (Nigeria Edition)

1. Do pension fees really affect my retirement savings?

Yes, and significantly. A 1% difference can reduce your final payout dramatically over decades.

2. Can low-fee PFAs still perform well?

Absolutely. Low fees do not mean low returns, efficient management matters more than high charges.

3. How do I know if my PFA is doing well?

Check their published returns, read your RSA statements and compare performance to industry benchmarks and PENCOM reports.

4. How often should I check my pension?

At least once a year and preferably quarterly if you can.

5. Is it safe to choose aggressive growth funds?

Yes, if you are young. Aggressive funds carry more short-term volatility but offer higher long-term growth potential and are managed by professionals.

Conclusion

Choosing the right pension company in Nigeria is more than a financial decision, it’s a decision about the life you want in retirement. Low fees protect your savings while high growth helps your money multiply over time. When these two qualities come together, you build a reliable path to a comfortable retirement.

Whether you are 25 or 55, the best time to start preparing for retirement is now. A good pension today is peace of mind tomorrow.

The write-up is as interesting and revealing as it can get on the subject matter under review.

Thank you Hon Ukende for ‘omprehensively putting this down for public consumption.