")

There is a belief in Nigeria that low income earners cannot be able to save money and can hardly build an emergency fund in Nigeria for themselves. I have personally witnessed someone who tried to break this myth and he succeeded in doing so. Let me share his brief story before we continue.

- Introduction

- What is an emergency fund?

- Why should Nigerians build emergency fund?

- How to build emergency fund in Nigeria in 7 steps

- Step 1: Calculate the exact amount you need

- Step 3: Open a Separate High-Yield Savings Account

- Criteria for choosing the right app

- Step 4: Automate Your Savings

- Step 5: Reduce Non-Essential Spending to Boost Your Fund

- Step 6: Increase Income Streams to Accelerate Your Savings

- Step 7: Protect the Fund and Avoid Temptation

- Common mistakes Nigerians make when building emergency fund

- Conclusion

A civil servant with just a meager salary of only N50k per month. He joined a savings (a contributory savings where people of the same age group come together to save money for a particular goal).

He had to start a barbershop to help compliment his monthly earnings and through the barbershop was able to start saving money from his N50K monthly earnings.

He had to split the N50K into three portions, one for the emergency fund which he was saving N5k monthly. The other portion (N20K) was to service a loan he took to buy the car he is using at the moment. The remaining N25K was saved through piggyvest (a FinTech app for saving and investing money).

Introduction

The state of the Nigerian economy needs everyone both young and old to plan things ahead of time especially when it comes to finances. According to data from the United Nations Food Program published last year (2024) shows that approximately 33.1 million Nigerians were projected to be pushed into food insecurity this year (2025).

Building an emergency fund in Nigeria cannot be all that easy but there are some strategies which when adopted could actually yield the desired result.

The reality of our economy is that, it is not favorable to anyone so it is important to start building an emergency fund in as soon as possible as a citizen to help cover for unplanned expenses.

Most Nigerians do not have a savings culture, as such, they tend to believe that it is not possible to save money with low income status. But with the experience I had with the civil servant whose story I narrated earlier, it may be possible if we structure our resources well and for that purpose.

What is an emergency fund?

Just as the name implies, an emergency fund can be defined as the amount of money that is saved or set aside to primarily cover certain unplanned or unexpected expenses.

These expenses may be a health challenge, auto repair, job loss or any other unforeseen circumstances.

Inasmuch as we may not be able to avoid or prevent those circumstances most times from happening, we can plan ahead of time before they happen.

Why should Nigerians build emergency fund?

Nigerians need to build emergency fund to help them mitigate the effects of the economic hardship being felt across the nation.

Inflation remains one of the key reasons why we as Nigerians should consider building emergency fund.

The purchasing power of the Naira has depreciated a lot, so building emergency fund could just put you on a safer side.

Emergency funds could also help tremendously when one loses his or her job, you have to use your the fund to help sustain yourself until you get another job or another source of income.

How to build emergency fund in Nigeria in 7 steps

Step 1: Calculate the exact amount you need

It is very important to know how much you need for a particular goal you hope to achieve.

So to calculate all your monthly costs currently in Nigeria, the first thing to do is to try to list all the fixed expenses which may include rent and debt repayments, and thereafter proceed to calculate the average monthly cost for the variable expenses which could also be listed as transport fare, food, and most times data subscription.

Some of the costs are only periodic, for example annual medical bills, which could be divided by the total 12 months to get the exact monthly figure, then summed everything together to find your total monthly expenses.

To properly calculate your needs Follow these steps:

1. List all your fixed expenses: fixed expenses are those remaining unchanged throughout the year such as debt repayments and rent.

Example:

Rent: ₦400,000

Debt repayment: ₦120,000

2. Calculate variable expenses: Variable expenses are those that change monthly such as food items, groceries, transport fare, airtime and data subscription.

Example:

Food: ₦45,000

Groceries: ₦75,000

Transport fare: ₦26,000

Data and airtime: ₦20,000

These are only estimated figures, they may not represent your exact spending.

3. Account for periodic expenses: Did you know that some of the expenses do not occur frequently such as medical check-up and even family celebrations like birthdays and some cultural festivals.

For instance: Healthcare could be ₦80,000 per year, which could translate to ₦6,666 monthly, that is if you work it out this way (80,000 ÷ 12).

4. Add up all expenses: Now we just need to add the entire monthly figures from all categories of expenses to realize the total monthly cost.

For example, rent + debt + food + groceries + transport fare + data subscription and airtime + medical check-up (₦400,000+₦120,000+₦45,000+₦75,000+₦26,000+₦20,000+₦6,666 = ₦692,666).

Step 3: Open a Separate High-Yield Savings Account

It is not advisable for you to deposit emergency fund in your regular and spending bank account, because you may be tempted to use it even when the need for it has not yet come.

it is more appropriate and safer to open a high yield savings account separately from your spending account.

This way interest will be accumulating on your savings and you won’t touch the money especially if you didn’t activate mobile transfers and USSD on the said account.

There are several FinTech apps which you could use to save your emergency fund, these apps are not the best but based on customer reviews I decided to list, always do your own research. The apps are;

- Palmpay

- Carbon

- PiggyVest

- Cowrywise

- Opay Save

Criteria for choosing the right app

Do not just choose an app because it looks beautiful to your eyes but based on what the platform has to offer. In this context, I chose the above platforms because of:

- Savings duration: Not all platforms offer seven days, one month, two months, three months and even seven days and even two weeks. So these apps have custom savings duration.

Safety: always do your own research before saving building emergency fund in Nigeria.

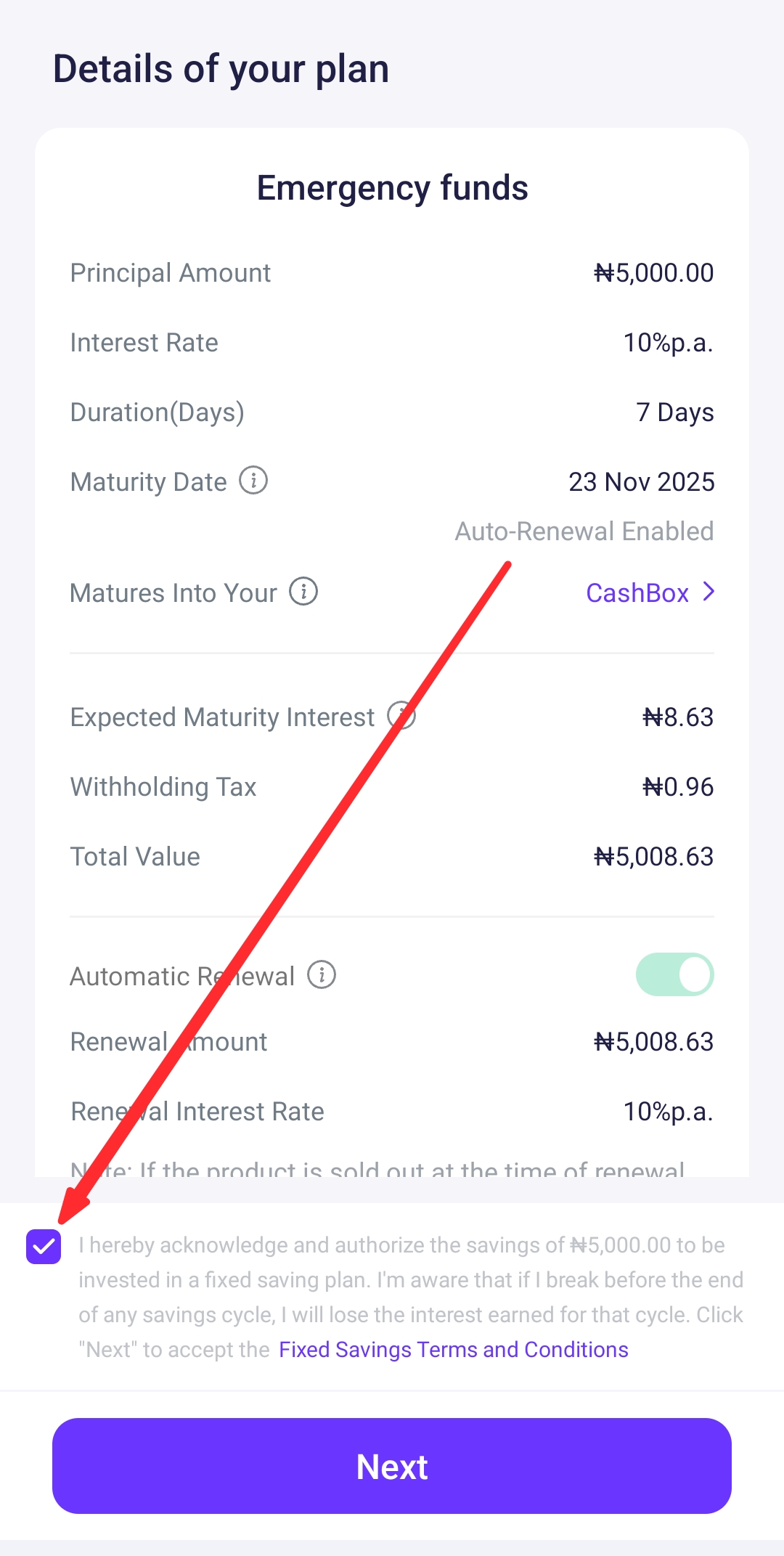

Step 4: Automate Your Savings

There is a need to automate your savings to avoid forgetfulness. There are some people that can easily forget when they are supposed to make deposits for the savings, so instead, they should automate it to allow the apps to deduct whenever the time for it is due.

To automate your savings, kindly follow the steps I highlighted below 👇:

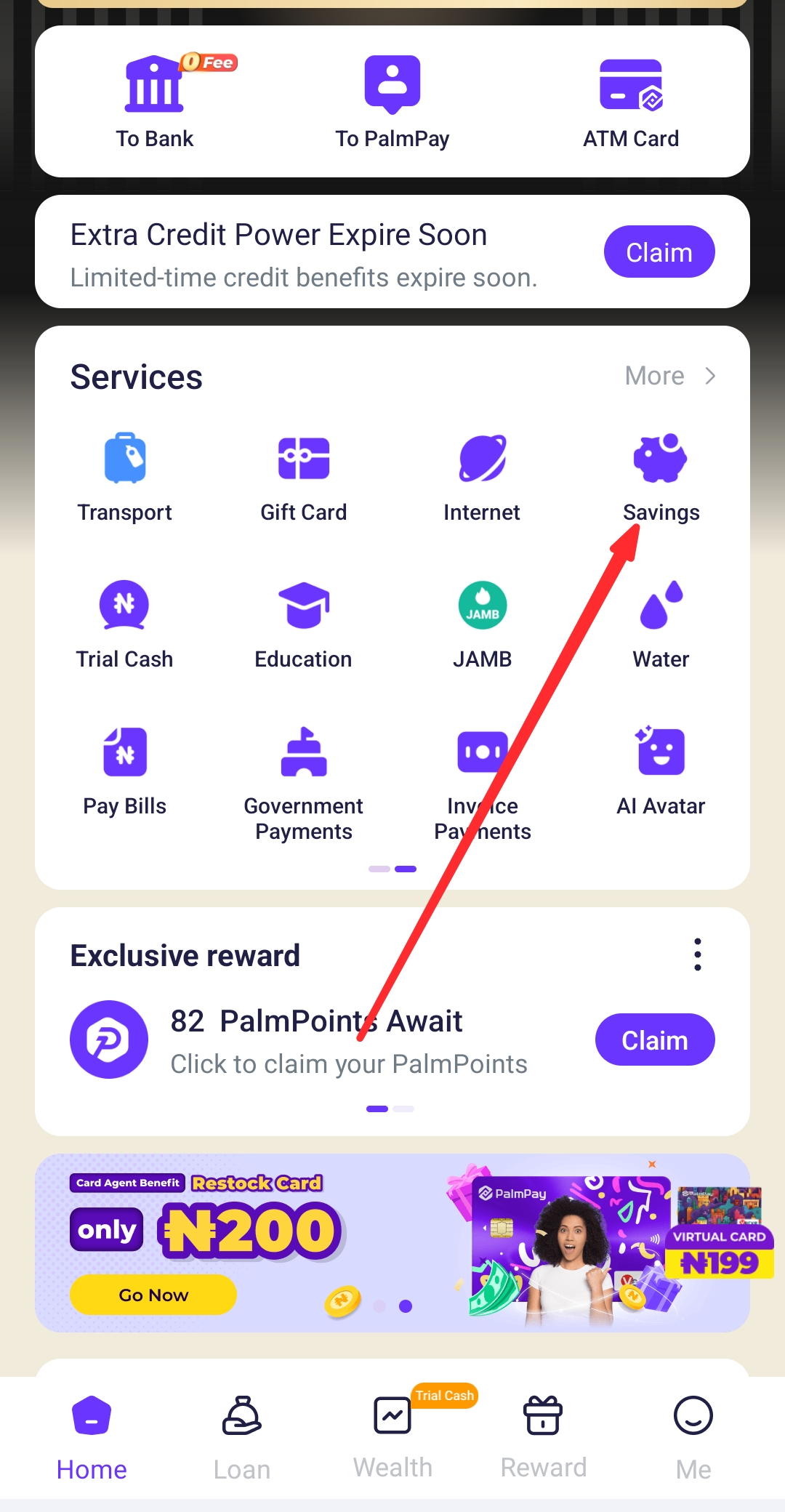

Step 1. login to your app: I’ll be using Palmpay for illustration, so login to your Palmpay app.

Step 2. Navigate to Savings: after you have successfully logged into your app, click on the “savings” labelled with a piggy icon.

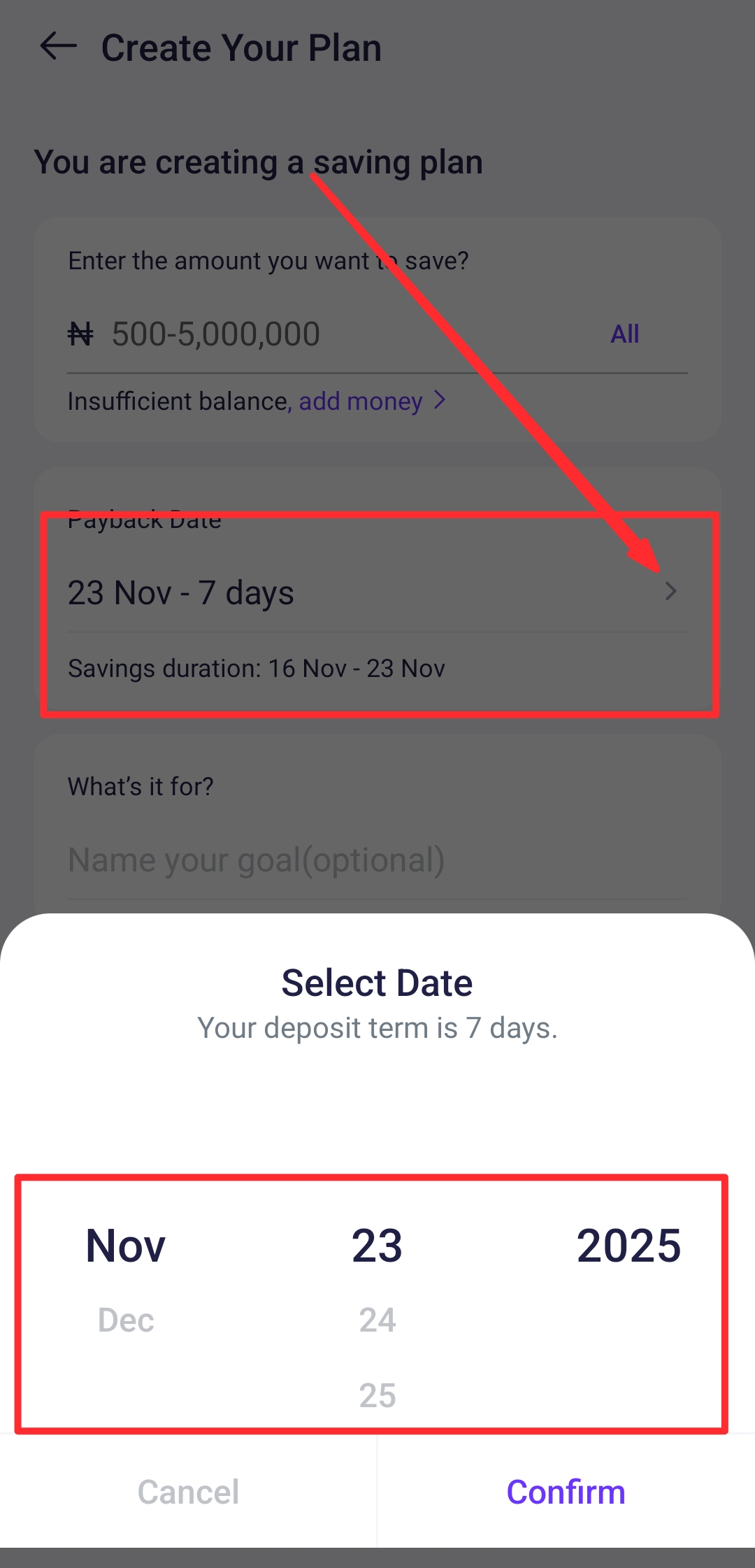

Step 3. Specify Savings duration: just go to the savings duration and click on the button that looks like a “greater-than sign”, then a rolling calendar will display. Select when you want your next automation should reoccur. For example five days, seven days, thirty days and so on.

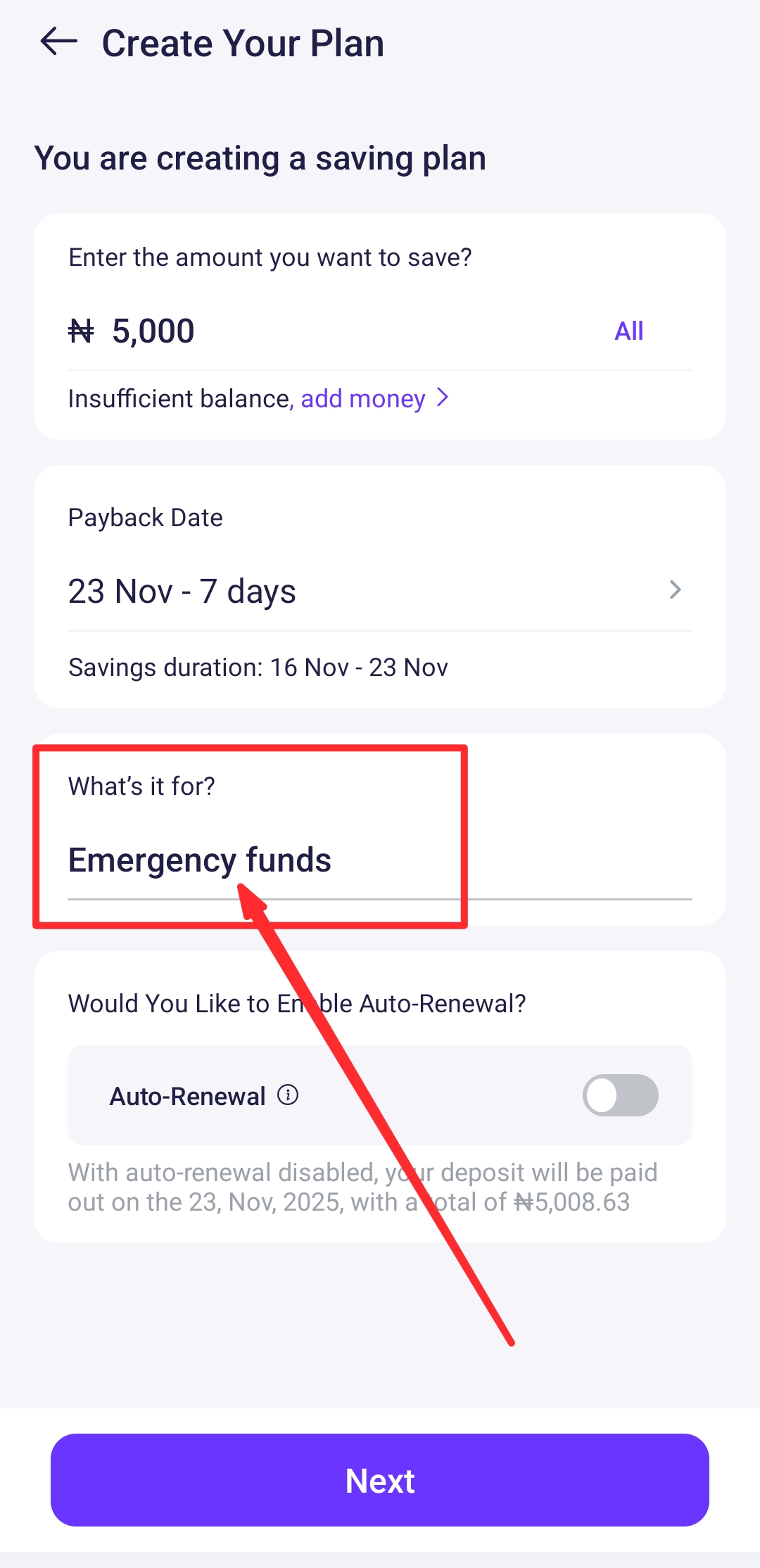

Step 4. Provide a name for the automation: this is optional but in case you have other automated savings, then specify each one with a name. The name could be the goal for the savings, for example “emergency fund”.

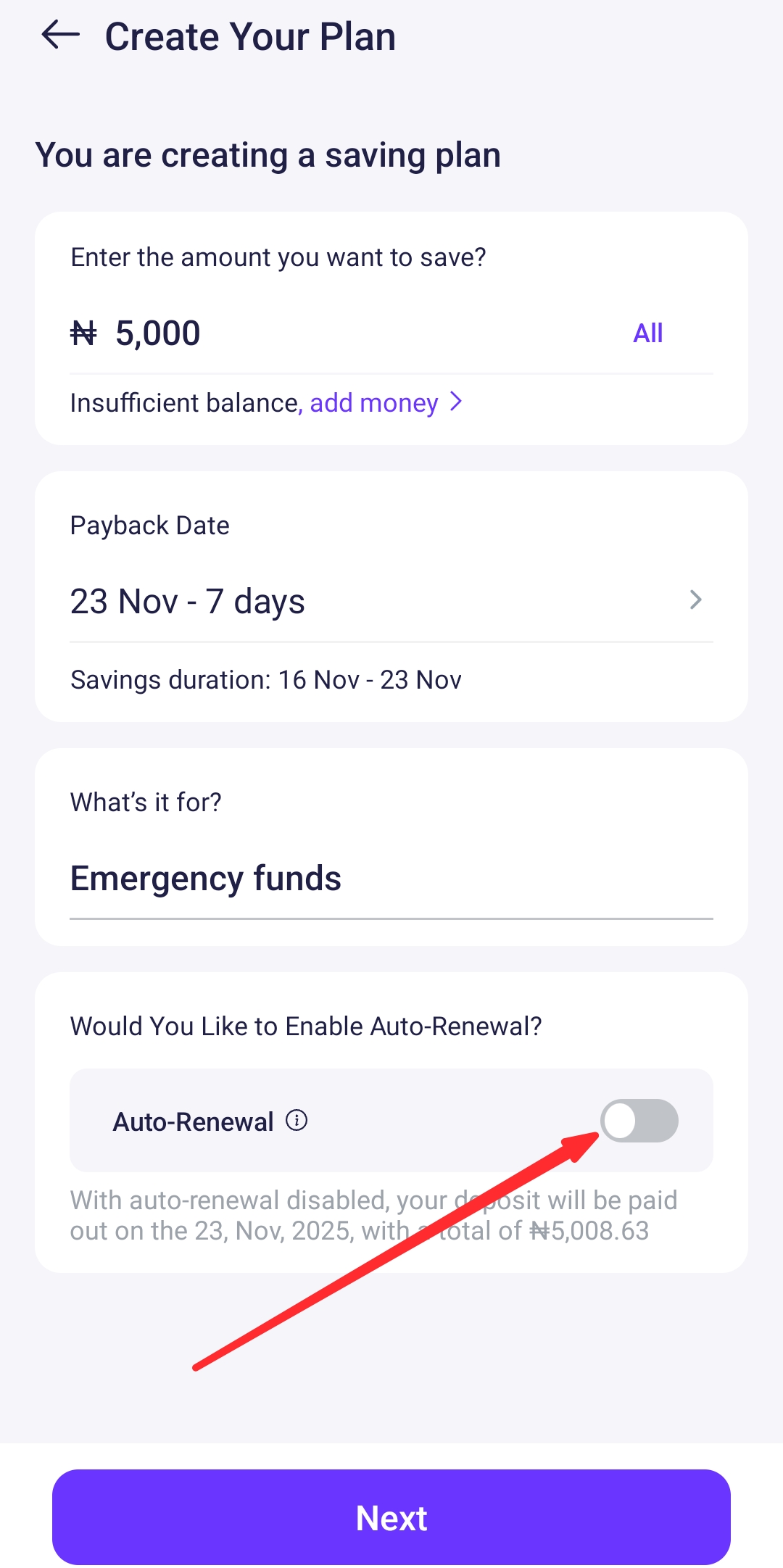

Step 5. Activate auto renewal: this button is very important, it normally tells that you want the “auto save” to continue after every seven days or as you have specify in the duration you selected. It will keep on renewing until you decide otherwise.

Step 6. Agree to terms and conditions: lastly before you preview and confirm, check the box for the terms and conditions. When you click in the box it will mark as you have accepted the terms and conditions.

Safety tips

- Do not be in a hurry to automate your savings in order to avoid errors.

- Take your time and be sure that you have written the right and intended figures for the automation and the “auto renewal button” is toggled properly.

Step 5: Reduce Non-Essential Spending to Boost Your Fund

To boost or increase your regular savings for the emergency fund in Nigeria, you have to check and adjust your spending habits.

Reduce the habits that encourages spending for non-essential things especially those that have alternatives that can be done with a minimal budget.

For example, eating outside or buying food in a restaurant at such a high cost, instead, cook at home and eat for many days at the same cost. This will help you save money.

Again, you can opt for a cheaper data subscription to save cost. You can also cut down unnecessary travels and holidays too.

These non-essential things when put into consideration can help you manage your low income and help you build emergency fund successfully.

Step 6: Increase Income Streams to Accelerate Your Savings

When you have multiple income streams, it will be easier for you to build and maintain emergency fund in Nigeria especially in this current economic reality in the country.

Take up some side hustles to help increase your income and also spread them. Side hustles are not hard to start so consider starting one today, such as:

- Freelancing: Avail yourself to be hired for a particular job that you’re skilled in and be paid at the end of it.

- POS: you can approach a bank and collect a POS for free or alternatively, buy it from Monie Point agents or Opay.

- Cleaning services: start cleaning services by buying those equipment and advertising on social media, you don’t need an office for this. Keep your gadgets at home and make use of them when you are being hired for a job.

- Mini import business: you can easily and with small amounts of money, buy things from China especially and resell in Nigeria to generate income.

- Real estate agent: this kind of side hustle does not require capital to start, just meet a landlord or property owner and discuss with him or her that you can provide them with a tenant. The potential tenant will have to pay you 10% of the tenancy fee.

How to divide extra income

Let’s just say you were able to start a side hustle, it will be of great importance if you divide your extra income and keep each portion for what it’s meant for or what you should do with it.

For example, you may say 50% fund, 30% bills, 20% enjoyment. This proportion is not a bad one but always do your own research.

Step 7: Protect the Fund and Avoid Temptation

One of the factors that makes it hard for low income earners to build emergency funds in Nigeria is the temptation to use the money when the need for it hasn’t yet come.

To protect the emergency fund and to also avoid the temptation of spending it before due time, always do the following:

- Use cash for in-store purchases: Don’t pay for purchases you have done in stores or anywhere within your locality with a debit card or transfers. Use cash because you know what you need to buy, you withdraw the exact cash for it, if the cash is exhausted, go back home.

- Don’t spend more than you budgeted: this is the kind of financial discipline that those who want to build emergency fund have. What you did not budget for, please don’t buy it even if you find it attractive.

- Use inaccessible accounts: the account you dedicated solely for the emergency fund should not be the type that you can have access to at any time. When you cannot have regular access to the account you may decide not to touch the funds again.

- Avoid hanging out with friends who are extravagant: there are friends you must avoid if you really want to save money for a particular goal. Those that motivate you to spend even when you do not budget for it. They may not have the same goals as you so avoiding them may help you save what you didn’t plan.

The emergency funds are meant for only emergencies, so as such only when you have such situations that you should use them.

Common mistakes Nigerians make when building emergency fund

These are so many mistakes that people often make when they want to build emergency fund in Nigeria. These common mistakes are as follows:

- Saving without tracking expenses: it is not a good idea to save without tracking your expenses because after a while you may still need to withdraw from it again because you forgot to set aside some money for your daily, weekly or monthly expenses.

- Keeping the money in a spending account: when your emergency funds are not deposited in a separate account meant for it, you may end up spending them. So try to separate your savings from the money meant for spending.

- Trying to save too much at once: almost similar to saving without tracking expenses, don’t save all your earnings at once, you have other needs that must be attended to as well, so doing so may result in giving up on it entirely in the long run.

- Zero income diversification: when you diversify your income, you will always have money to save. It is not a guarantee that your employer will pay salaries this month, he may owe you but you must be debited for the savings this same month, therefore, you may end up being disappointed. This won’t be the same case if you had diversified your income. When one source fails the other may complement.

Conclusion

Despite the current economic situation of Nigeria, and even with a low income you may be able to build emergency fund in Nigeria. All you need to do is to start small and take a step towards it, before you know it you may have started saving already.

Always remember that diversification may help you achieve the goal of building emergency funds without much stress.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. WatchNigeria is not responsible for any losses arising from reliance on the information provided. Always conduct your own research or consult a qualified professional.

: Complete Step-by-Step Beginner’s Guide")

")